What Are Principal Protected Notes In Canada? Everything You Need To Know

Image Source: Pixabay

It is an investment that offers both principal and interest investors by banks and other financial institutions. PPNs allow investors to avoid worrying about the conditions of the market and focus on their financial objectives. Keep reading to know more.

What Are Principal Protected Notes?

Principal protected notes (PPN) are fixed-income securities that provide guaranteed returns. These are designed to protect your principal investments and give you a handsome return after a certain time. These PPNs have a term of 7 to 10 years. The return you get from investing in PPN is linked to a specific index’s performance. The investment can be in mutual funds, hedge funds, stock markets, or commodities such as oil.

What Are The Associated Risks?

Here are some of the risks associated with PPNs.

1. Interest Rate Risk

Interest rate changes can affect the net asset value (NAV) of a PPN. When interest rates are low, the NAV is high. At or near par, the NAV can be low. This can be due to declining trust in the PPNs’ ability to handle the increased interest rate risk.

2. Fee Risk

The combined fees charged might be higher than the return you will receive. It is important to consider your PPN fees when deciding if the product is the right fit for you. There are many ways your PPN could charge fees. You can be charged with fixed fees, asset protection, servicing, and other fees associated with holding financial assets in an account.

3. Liquidity Risk

Liquidity risk is a major risk of investing in PPNs, as it happens when the investor has to sell the PPN before maturity. In the event of a term deposit or a fixed-term bond, the investor must liquidate the asset before maturity and reinvest the proceeds in another PPN.

What are the Advantages and Disadvantages?

Advantages:

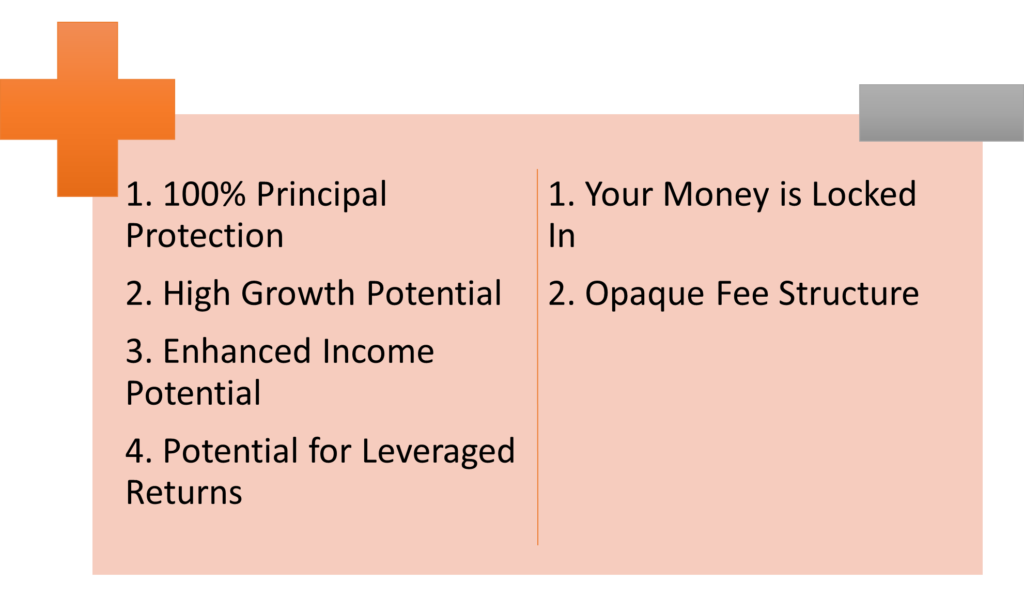

1. 100% Principal Protection

- Regardless of the performance, you will be receiving your full principal amount at the time of maturity.

2. High Growth Potential

- The most crucial benefit of PPNs is the potential for significant growth.

- If you follow the rule of thumb, you want to put your money in safe assets with a respectable rate of return.

- But, with PPNs, you can earn significantly higher returns.

3. Enhanced Income Potential

- Enhanced income potential is always an advantage.

- PPNs can help you get more money for the products you are promoting.

- PPNs help you earn a predictable amount of income.

4. Potential For Leveraged Returns

They can be leveraged to create a return beyond just the interest rate paid. You could get a PPN bearing a higher yield than a traditional investment.

Disadvantages:

1. Your Money Is Locked In:

- When you invest in a PPN, you lose the ability to pull out your original investment.

- If you want to get your money out sooner than projected, you will have to pay penalty.

- There is also the risk of losing the guaranteed interest rate on your principal.

2. Opaque Fee Structure

- The primary disadvantage of PPN is that the fees are not clearly defined upfront.

- This makes it difficult for investors to determine the cost of the investment and the amount they will receive in return.