Top Things to Know About the Dark Side of Fintech Borrowing

In this modern world, technology is at its peak; the internet has connected people bringing them closer to each other and bypassing all geographical boundaries and limits. It all started with making social connections online, but now its scope and reach have expanded to finance and how businesses raise funds

.

The term “Fintech,” Finance plus technology, was coined recently to represent all the borrowings and disbursements made via the internet route. The digital lenders under this ambit use cutting-edge technology and artificial intelligence to raise funds.

Some prominent fintech companies in Canada are KOHO Financial, Borrowell, Bitbuy, NDAX, Nesto, Neo Financial, et cetera. All these business organizations use technology as their primary weapon when it comes to raising as well as distributing loans.

Indeed, it is a revolution in the finance sector, but not everything is as rosy as it seems. For some consumers fintech borrowing offers them the worst experience. We certainly need to know its dark side.

Why Fintech Borrowing Is Not Good?

There are several reasons why fintech borrowing can prove the worst for you. They are:

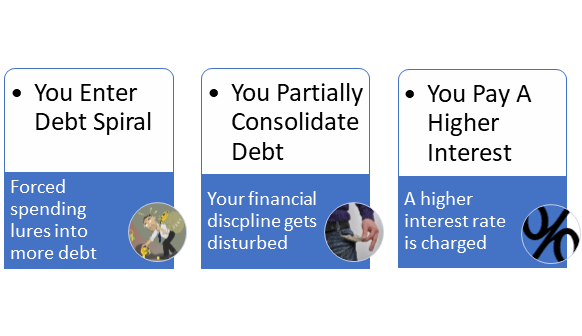

1. You Will Get Caught in the Debt Spiral

Recently, a research conducted on a group who availed loans from fintech companies showed astonishing results. It established that:

- Forced Spending

- With easy credit available, you get encouraged to spend more – even beyond your means.

- It disturbs your psychological process and sanity. You bypass rationality and the general sense of frugality.

- It also impacts your savings and diverts you from your financial goals.

- More Debt

- The fintech companies are less stringent when it comes to extending loans to their customers.

- If you are not getting a loan from the big five traditional Canadian banks, you can reach them.

- With lenient provisions and easier credit evaluation processes, you will likely get a loan, albeit at a higher interest rate.

- This way, you will assume more debt than you need and sink further into the debt trap.

- Higher Defaults

- This study also found that people who took loans from fintech companies defaulted more often than people with similar credit profiles borrowing from traditional banks.

- It holds as fintech borrowing is more expensive compared to traditional.

- The big banks enjoy economies of scale and have a wider customer reach, which allows them to obtain funds at a cheaper rate, as compared to the new age fintech companies.

- When you take a loan from fintech company, you usually have to pay a comparatively high-interest rate – This hurts your monthly budget and, in a matter of time, you may default.

2. Lack of Debt Consolidation

Firstly, let us understand what debt consolidation is. It is common for borrowers to assume multiple debts, such as car loans, personal loans, credit card balances, mortgage loans, etc.

Using debt consolidation, you can manage your finances better by reducing your debt burden. You can do this by taking a loan at a lower interest rate to pay off single or several existing high-interest-rate loans.

For example, let us assume that you have three different outstanding loans, which are:

- Credit card loan of $15,000 at 24% p.a.

- Personal loan of $30,000 at 17.5% p.a.

- A car loan of $20,000 at 12% p.a.

You are always regular in paying your EMIs and have never defaulted. It improves your credit score, and you get a $65,000 loan from a leading traditional bank at 10% p.a.

Using the debt consolidation technique, you will take this 10% p.a. loan and pay off all your existing loans.

It has been widely observed that fintech borrowers only partially consolidate their debts. Initially, they practice debt consolidation, but only after a few months do they start available credit card lines.

Their financial discipline goes for a toss, and they again start buying consumer goods, cars, and even everyday items using debt. This behavior is financially bad and not prevalent among the borrowers of traditional banks.

3. You Will Pay More Interest

What separates different loans? – Unarguably, it is the interest rate. You will always prefer to obtain a loan, which is cheaper, that has a lower interest rate.

But this is not the case with fintech borrowing. Undoubtedly, the fintech companies are growing and disbursing more loans than ever. But this also brings a higher default risk due to their practice of giving loans to people with a “thin” credit profile.

Yes, your application gets rejected by the big banks. No worries, you can turn up to fintech lenders. It prompts them to charge a higher interest rate to their borrowers.

A premium of 5% is quite common in this space – This means if you can get a loan from traditional banks at 4% p.a., you will be required to pay 9% p.a. for fintech loans.

It increases your interest cost substantially and lays considerable stress on your finances.