Are Private Mortgage Lenders a Good Option for Borrowing?

Many people need to borrow money when buying a home because they may not have enough savings. However, traditional bank loans can be overwhelming with lengthy approval processes and strict loan terms.

In such scenarios, private mortgage lenders have emerged as a compelling alternative to the traditional banking route in Canada.

In 10 quarters up to September 2022, Canada’s private mortgage market share surged by 45%, according to the latest data from CMHC. It means that more than one in 10 Canadian mortgages are now provided by private lenders.

But are they really a good choice for you?

Let’s discover if private lending is the key to your dream home. By the end of this post, you’ll understand the pros and cons of working with a private lender, helping you make a wise financial decision.

Who are Private Mortgage Lenders?

In simple terms, private mortgage lenders are individuals or companies that offer loans outside traditional banks. Banks are heavily regulated and have strict requirements for loans. However, private home loan lenders have more flexibility in their lending practices.

They can be real estate investors, private equity firms, or even wealthy individuals who are looking to invest their money. They may have varied loan approval criteria and could help borrowers who are unqualified for traditional mortgages.

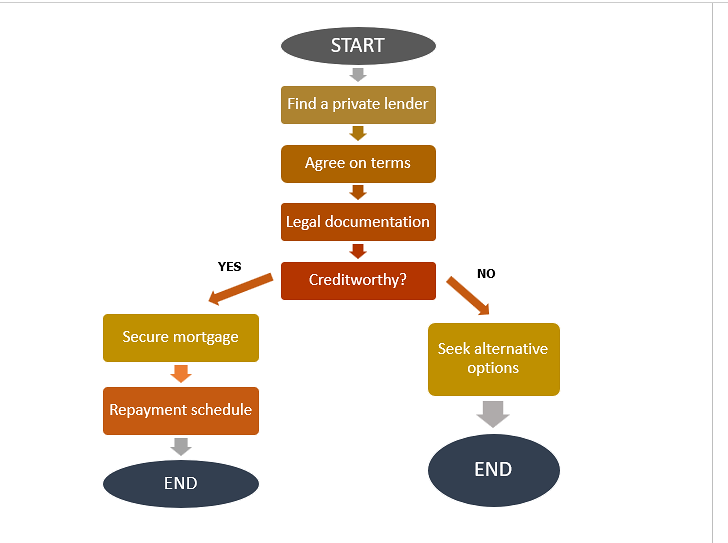

Here’s a simple flowchart showcasing how the system of private home loan lenders works in Canada?

What are the Advantages of Using Private Mortgage Lenders?

Here are a few reasons why a private mortgage lender might be a good choice:

- Faster Approval Process

One of the main benefits of working with the best private mortgage lenders is the speed of the approval process.

Traditional lenders often have a lengthy application process. They usually include multiple stages of approval and documentation requirements.

Private lenders, on the other hand, have a more streamlined process. This means that customers can get approved for a loan much faster.

- Flexible Lending Criteria

As mentioned earlier, private home loan lenders have more flexibility in their lending criteria. They may assist borrowers with imperfect credit, irregular income, or other factors that could disqualify them from a traditional mortgage.

This can be especially helpful for self-employed individuals. It can also be beneficial for real estate investors or those who have experienced financial setbacks in the past.

- Customizable Loan Terms

Private home loan lenders often have the ability to customize loan terms to fit the borrower’s needs.

This can include things like loan amounts and interest rates. It can also involve repayment schedules and even the duration of the loan.

This flexibility can be particularly useful for those who don’t fit the mold of a traditional mortgage borrower.

What are the Disadvantages of Using Private Mortgage Lenders?

Here are some of the weak points of this type of lending:

- Higher Costs

The major downside of using a private mortgage lender is the higher costs associated with the loan. Private lenders often charge higher interest rates and fees compared to traditional lenders. This can make the overall cost of the loan more expensive, which is something you’ll need to consider when weighing your options.

- Potential for Predatory Lending Practices

Unfortunately, the lack of regulation in the private lending industry can also lead to predatory lending practices. Some private lenders may try to take advantage of borrowers by charging hidden costs or imposing unfair terms.

- Fewer Protections for Borrowers

When you borrow from a traditional lender, you have certain legal protections and recourse options if something goes wrong. With private home loan lenders, these protections may be more limited, so you’ll need to be extra careful when reviewing the loan terms and documents.

Private Mortgage Lender Vs. Traditional Mortgage Lender: Tabular Comparison

| Component | Private Mortgage Lender | Traditional Mortgage Lender |

|---|---|---|

| Approval Process | Faster and more flexible | Lengthy and stringent |

| Loan Terms | More negotiable | Standard and fixed |

| Interest Rates | Higher rates possible | Lower rates |

| Credit Requirements | Less strict | More stringent |

| Documentation | Less paperwork required | More documentation needed |

| Down Payment | Flexible options | Fixed percentage required |

| Loan Amount | Higher maximum possible | Standard limits |

| Repayment Schedule | More flexible options | Fixed and structured |

| Borrower Eligibility | Non-traditional situations | Conventional borrowers |

| Customer Service | Personalized approach | Standardized service |

Is a Private Mortgage Lender Right for You?

Deciding whether a private home loan lender is the right choice for you will depend on your specific financial situation and borrowing needs.

Here are some key factors to consider:

- Credit History and Score: If you have a good credit score or a non-traditional credit profile, a private lender may be more willing to work with you.

- Income and Employment: Private lenders may be more flexible with irregular or self-employment income.

- Property Type: Private lenders may be more open to financing non-traditional properties, such as investment properties or fixer-uppers.

- Loan Amount: Private lenders may be able to provide larger loan amounts than traditional lenders, especially for investment properties.

- Timeframe: If you need to secure financing quickly, a private lender’s faster approval process may be beneficial.

It’s important to carefully weigh the pros and cons and compare offers from multiple private mortgage lenders to ensure you’re getting the best terms possible.

What are Some Tips for Working with Private Mortgage Lenders?

If you do decide to work with a private home loan lender, here are some tips to help ensure a smooth and successful experience:

- Understand the Loan Terms: Carefully review all the loan documents and make sure you fully understand the terms, including the interest rate, fees, repayment schedule, and any potential penalties or prepayment clauses.

- Research about the Lender: Before signing any agreements, make sure to research the private lender’s reputation, credentials, and past track record. Look for reviews, references, and any complaints or legal issues.

- Have a Backup Plan: Consider having a backup financing option in case the private loan doesn’t work out or you need to refinance in the future. This could be a traditional mortgage or a line of credit.

- Don’t Forget to Compare: It’s always a good idea to explore different lenders and compare their rates and terms to find the best deal.

The Concluding Lines

Private mortgage lenders can be a viable option for borrowers, especially those who are not eligible for traditional loans. They offer you more flexibility, faster approvals, and a lending experience tailored just for you.

However, it’s equally important to be cautious to ensure you’re working with the best private mortgage lenders. By understanding the risks and benefits, you can make an informed decision about whether a private mortgage is the right choice for your borrowing needs.