Understanding Home Equity Lines of Credit (HELOCs) in the GTA: Benefits and Considerations

Introduction:

For many people and families, becoming homeowners marks an essential turning point. Your house is a precious asset that you have as a homeowner. When you pay off your mortgage and your home’s value increases over time, you build equity. A home equity line of credit (HELOC), a financial instrument, can be used to leverage this equity.

In this article, we will examine the advantages and factors to be considered with HELOCs in the Greater Toronto Area (GTA).

What is a HELOC?

A Home Equity Line Of Credit (HELOC) is a financial instrument that enables property owners to borrow money using the equity they have accrued in their house. It is a revolving line of credit with an established credit limit, much like a credit card. Homeowners can use their HELOC as required and simply pay the interest they borrow.

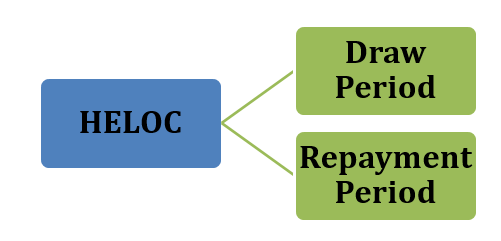

How Does a HELOC Work?

The draw time and the repayment period are the two regular periods of a HELOC.

- Homeowners have permission to borrow money from the HELOC during the draw period and make interest-only payments. Typically, the draw phase lasts five to ten years.

- Homeowners must start repaying the principle and interest over a predetermined length of time once the draw period expires, during which time they are no longer permitted to borrow cash.

Benefits of HELOCs in the GTA:

Credits: Pixabay

Access to Funds:

The easy access to cash that HELOC provides is one of its main advantages.

- Homeowners in the GTA can use the equity they’ve accrued in their homes to pay for a range of obligations.

- A HELOC can be an efficient financial instrument if you’re remodeling your house, paying for college, paying off higher-interest debt, or investing in other chances.

Lower Interest Rates:

- In comparison to other kinds of borrowing, including credit cards or personal loans, the interest rates for HELOCs are frequently lower.

- HELOC interest rates are frequently correlated with prime rates, making them more accessible to homeowners in the Greater Toronto Area. It may save a lot of money on interest over time.

Tax Advantages:

- If the borrowed money is utilized for investment reasons, the interest on a HELOC may be tax deductible in Canada.

- By maximizing their financial gains and lowering their overall tax burden, homeowners in the GTA may profit from this tax advantage.

- But in order to fully grasp the exact tax ramifications depending on unique circumstances, it is crucial to speak with a tax expert.

Flexibility and Convenience:

- HELOCs give homeowners access to a line of credit that revolving, allowing them to borrow, pay back, and borrow again as required.

- Homeowners in the GTA may better manage their budgets thanks to this flexibility, especially when expenses change or unforeseen bills appear.

- Homeowners may easily get money when they need it without constantly filling out applications.

Considerations for HELOCs in the GTA:

Changing Property Values:

- Despite recent substantial growth in property values in the GTA, it’s crucial to be considered the possibility of market volatility.

- The amount of equity accessible to homeowners might increase or decrease depending on the value of a property. It is critical to use prudence and responsible borrowing while considering prospective changes in property values.

Debt Build-Up:

- HELOCs make it simple to obtain money, but it’s vital to be aware of the risk of debt accumulation.

- Homeowners in the GTA should evaluate their capacity for responsible debt management and be sure that taking out a HELOC is consistent with their financial objectives and financial limits.

- It’s essential to have a clear strategy for how the borrowed money will be put to use and to stay away from utilizing the HELOC to pay for unneeded costs or non-appreciating assets.

Variable Interest Rates

- HELOCs frequently feature variable interest rates, which can alter in response to movements in the market, unlike regular mortgages.

- Variable rates have the possibility of rising over time, despite the fact that they may initially be cheaper.

- Homeowners in the GTA should carefully assess their financial status and take into account their capacity to handle anticipated interest rate changes.

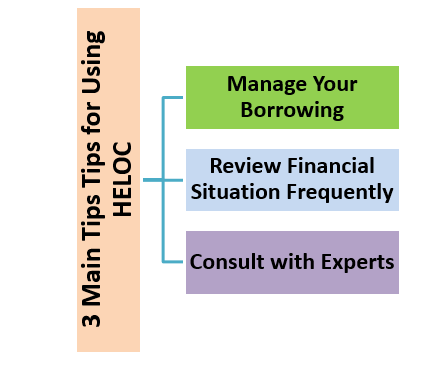

Tips for Using HELOCs Wisely in the GTA:

Conclusion:

In conclusion, a Home Equity Line of Credit (HELOC) may be a useful financial instrument for homeowners in the Greater Toronto Area (GTA) to access cash, benefit from reduced interest rates, and enjoy flexibility. However, homeowners must carefully to be considered elements like varying property prices, debt management, altering interest rates, financing requirements, and related expenditures. Seeking professional advice and making informed decisions are crucial to effectively leverage the benefits of a HELOC while minimizing potential risks.