Navigating The Complex World Of Mortgages

If you are looking for buying a dream home in Canada, you must avail the Mortgage service that most people tend towards while embarking on the journey of homeownership.

The Mortgage world is quite overwhelming for people that do not know the terminology, how mortgage works, and what are the prospects of using a mortgage to buy your dream home.

Without proper knowledge, it becomes difficult to navigate through the complex world of mortgages, but knowing some aspects of a mortgage will allow you to steer your journey to homeownership and you will find the perfect mortgage for your dream abode.

Basics of Mortgage

A mortgage is a loan from a lender using the property that you will buy as collateral.

The loan is for a tenure where you have to pay a principal, and the lender profits from the interest you pay till you repay that debt.

For you to get a mortgage, you must fulfill some requirements as:

- A healthy credit score.

- Minimum down payments that you can afford.

The Mortgage application has a rigorous phase before you will be able to borrow the sum of money for buying your dream house.

The two types of mortgages that you can opt for based on your needs are:

- Conventional Loans

- Fixed-Rate Loans

Conventional Loans

A Conventional Mortgage Loan is a type of loan from any financial institution or lender that you repay in the form of installments.

You can borrow a loan by using your house as collateral.

Conventional Loans or Variable Rate loan is the type of loan that you borrow wherein the interest rate is variable and depends on factors such as a credit score and a credit history.

More the credit score, the lesser the interest rate. If your credit history is blemished, you have a minimum chance of securing a loan. If your credit history is clean, financial institutions or lenders will have a clean image, and you can get a loan with a lesser interest rate.

Fixed-rate Loans

A fixed-rate mortgage loan is a loan where the interest rate remains the same throughout the tenure of the mortgage.

Opposed to variable-rate loans, where the interest rate can vary over time, a fixed-rate loan doesn’t allow that flexibility.

The bond market is closely linked with the rates of fixed mortgages, and is directly proportional to it.

The principal amount is also fixed if you choose a fixed-rate loan and no matter the tenure of the loan.

Overall Process

Whenever you opt for a mortgage, the financial institution or the lender that you seek for borrowing will check your credit history and credit score and analyze whether you are capable of paying back the loan that you owe.

If the lender seeks you fit, your application gets approved and the lender offers you a loan amount with a certain interest rate that you have to repay in a certain period.

Once the principal amount and interest rate are fixed a process known as “Closing” occurs. When the ownership changes to the buyer, the buyer then signs the remaining mortgage documents.

You have to pay the loan back until you have the property under your belt, having cleared all the debt.

The general mortgage term is 15 to 30 years.

Some options for where you can get a mortgage deal:

- A credit bank union

- Financial Institution (Banks)

- Mortgage-Specific lender

- Online-only lender

- Mortgage broker or agent.

However, you have to go through different options to get the best deal.

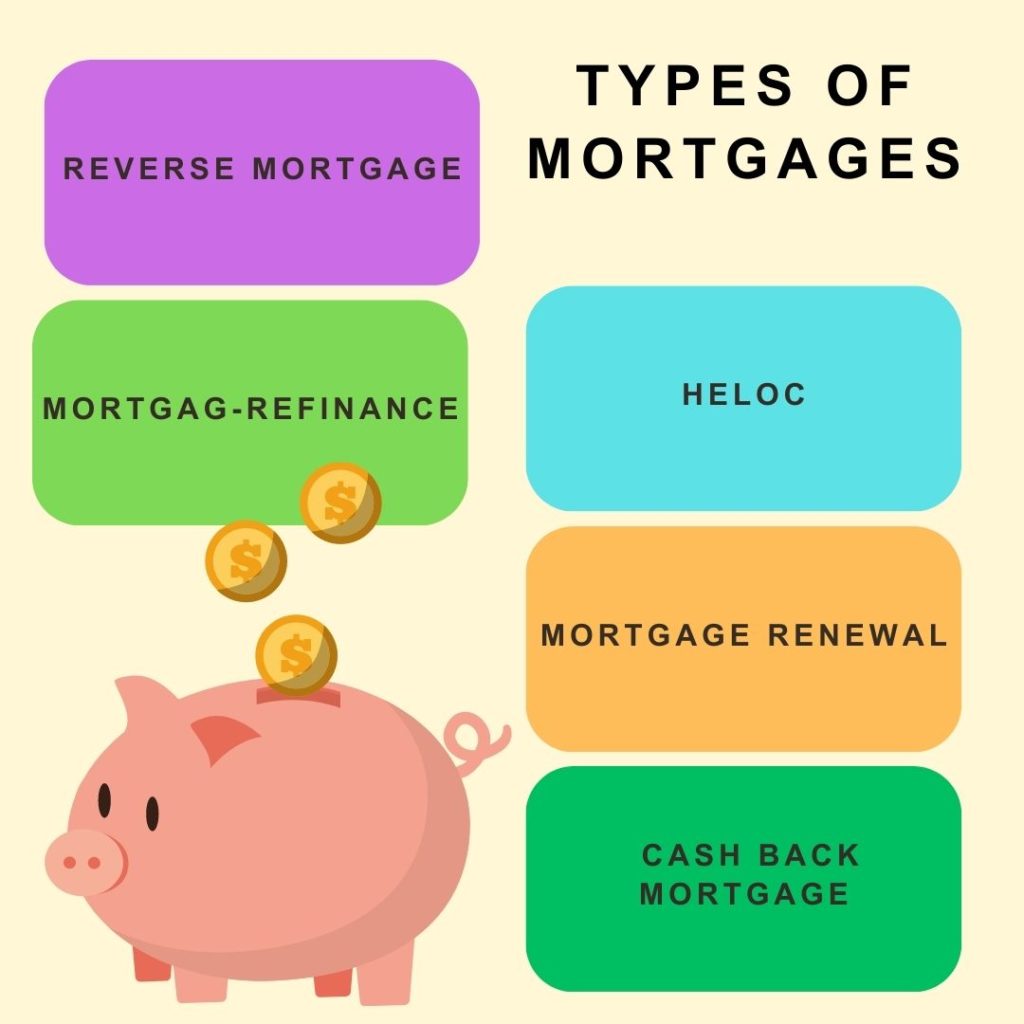

Types of Mortgages

Some types of mortgages are:

Mortgage Re-Finance

Mortgage Refinancing allows you to give credit at a lower rate than any form of borrowing by using your home equity as collateral.

A lower mortgage rate will allow you to achieve your financial goals and increase your savings gradually, which you can use anywhere.

It can also be used to roll over the enormous debt that is piling up before you, which leads to magnificent growth in your financial condition.

You can save thousands of dollars by Mortgage Refinancing.

HELOC

HELOC or Home Equity Line Of Credit gives you relatively low-interest rates compared to other lines of credit like credit cards or a loan by using your home equity as collateral.

A line of credit can be drawn from anywhere, and you are only required to pay interest with no fixed payment requirements.

You can pay the remaining balance in whatever way it suits you.

A HELOC is available to you as long as you own a home. You can use it as an emergency fund whenever you want.

Mortgage Renewal

A mortgage renewal can be a great opportunity and is as important as securing a first mortgage.

Without any penalty, you can renegotiate every aspect of your mortgage while renewing and can boost your savings.

Mortgage Renewal can help you merge your loans into a single mortgage which will get you a lower payment.

It also saves you extra interest costs and boosts your monthly cash flow

• You should review your available options six months before renewal as you can attain many great options in the market that I can provide you with.

• If you are thinking of gaining equity for any grand purchase, a mortgage is the best thing you can opt for.

Cash Back Mortgage

Cash Back Mortgage is useful when you buy a home and want extra cash for closing costs such as legal fees, land transfer taxes, or home inspection costs.

• If you are buying a home that needs renovation and do not want another loan, you can fall back upon a cash-back mortgage.

•If you prefer to have a cash buffer available for unexpected expenses or to address any financial challenges that may arise after purchasing a home. A cash-back mortgage can provide that extra cushion to ensure peace of mind

Reverse Mortgage

A reverse mortgage is the most flexible way for people aged 55+ that require financial assistance without selling any equity in their house.

•Your home equity is converted into tax-free cash that can allow you to repay all your debts and make you financially independent.

• It is the best way for elders to regain financial stability and steer their life toward their comfort zone.

Why do you need a Mortgage?

In the modern world, the real estate market is booming as the population is increasing, affecting the price of a house many people cannot afford.

Opting for a mortgage allows people to pay only a specific amount at the time of buying (Generally 20%), and the balance can be repaid by the loan you borrow.

If the owner is unable to repay the loan, his home is secured by the lender because it is collateral for the loan that the borrower gets.

Conclusion

A mortgage is an efficient way to buy your dream home if you are not sitting in a pile of cash. Your dream of buying a home can be achieved with the powerful tool known as a mortgage.